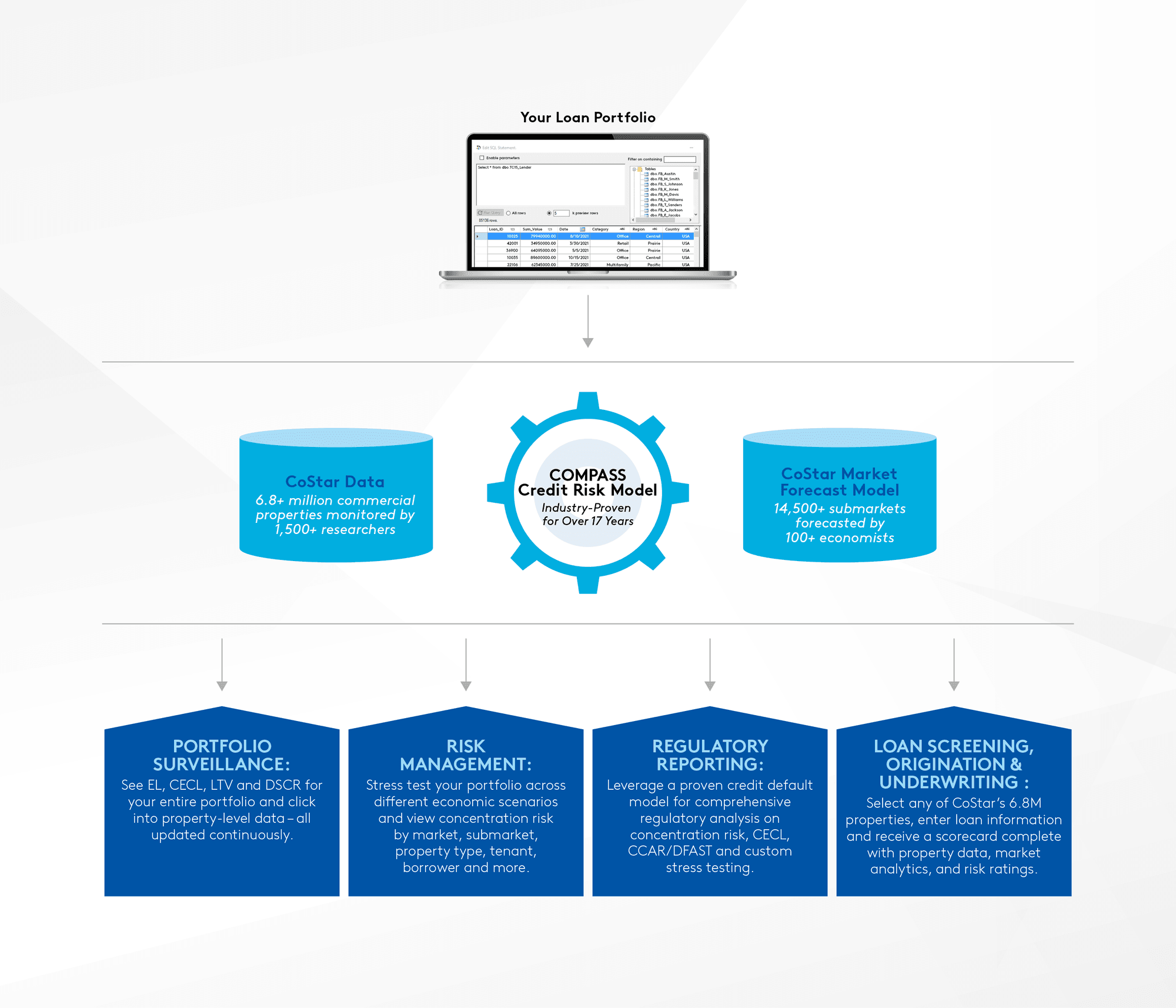

CoStar’s proprietary COMPASS credit default model is integrated into Costar for Lenders and has been trusted by regulators and large financial institutions for over 20 years.

Since COMPASS is powered by CoStar’s property information and market research, you’ll see LTV, DSCR, EL and CECL through the loan term and at maturity.

Click in the arrow on the right to learn how connecting your portfolio to the COMPASS credit default model and CoStar’s property information and market research gives you an edge at every stage of the lending process.

Developed based on sufficient,accurate and granular data

Captures the idiosyncratic risk characteristics of property, loanand local market

Adjusts for current and future market change with a forward-looking perspective

High computation power

Encompassed with all relevant data pointsto provide a holistic view in one platform

Detailed model methodology disclosure

Rigorous model performance test

Regulatory compliance on model risk management:– OCC Bulletin 2011-12 / SR 11-7– FIL-22-2017– CECL ASU 326/IFRS9– Basel III